A safe place to whine about everything you don’t like about economic policy and how you could do it better if you only had the chance.

feel free to give short questions, answers, or comments on any economic policy issue, subject to a few simple Club Rules: 1) no personal attacks, 2) no bad language. Violators will be deleted. (I’ll be the judge.)

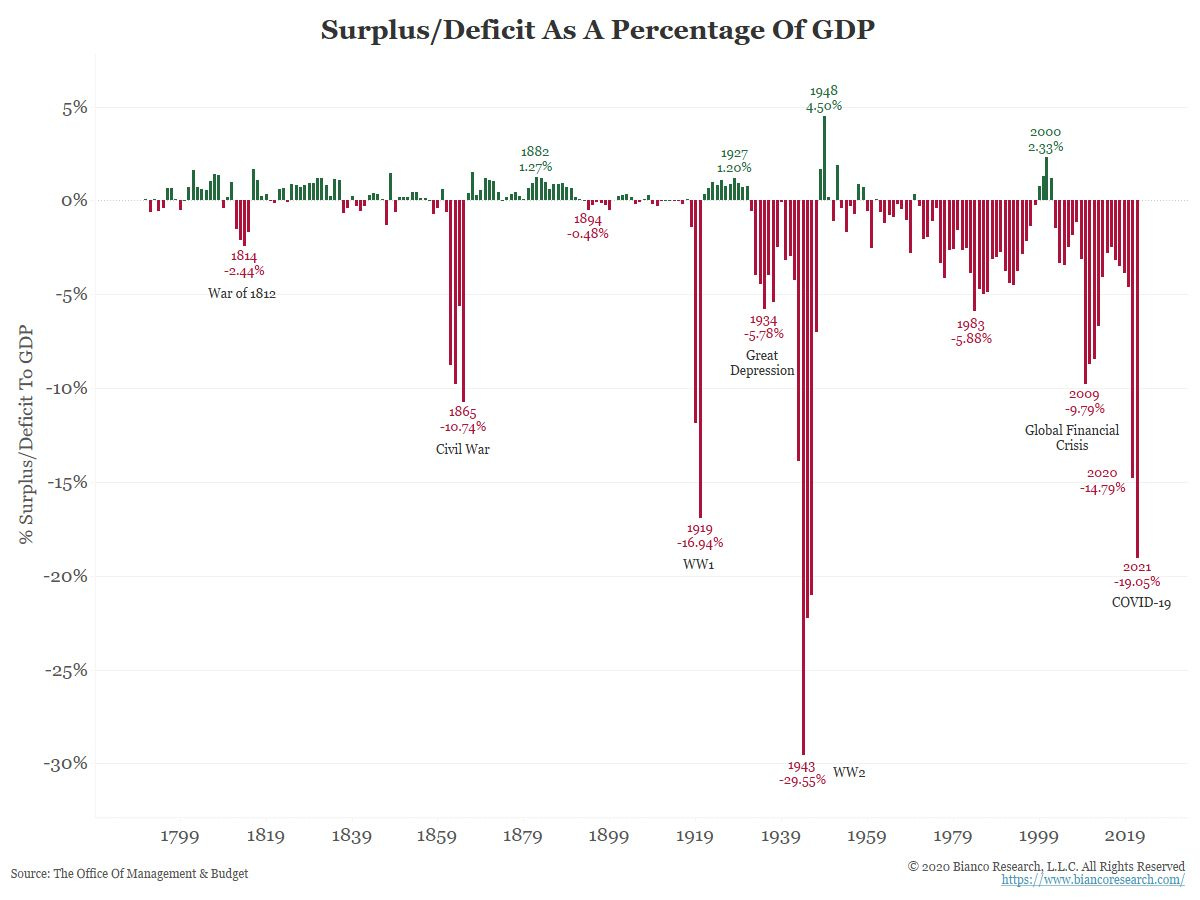

Here’s a chart to start off the discussion courtesy of James Bianco. What do you think is the implication of the budget deficit being 19% of GDP? Will it return to historical ranges? What happens if it doesn’t?

Oh, and on the implications of the chart: a budget deficit of 19% at a time of notional peace makes me think of Argentina, not the US. It will return to historical range when, but not before, a serious President is voted into office that understands how nations turn to ruin and decides not to take that route. If it doesn't, financial ruin follows. Don't cry for me, Argentina.

As a former rating analyst (sovereigns and corporates), I whine about how people think that interest rates are going to remain low forever. I've seen too many companies that are 200 basis points from insolvency, and too many countries who will lose their ability to actually have any discretionary spending because a 200 basis point interest rate increase for their debt will quickly force them into a strait-jacket of debt servicing.

I whine that no one seems to remember that debt is future consumption denied (Eugen von Böhm-Bawerk).

I whine that economists have forgotten entirely that economics is a living thing, and to live implies both imperfection and change (Lüdwig von Mises).

I whine that productivity is vastly underreported because even the best hedonic deflators fail to capture the improvements in quality of life and work.

I whine that no one went to jail for the sheer insanity of sub-primes, least of all anyone from the rating agencies.

I also whine about how hard it is to get back into shape after the age of 50, but not even my wife listens to that one.

John, I bow before you and declare you to be the one and rightful Whine-master General for your all-encompassing summary. Each one of them could be an essay in its own right. I look forward to discussing them with you along the way.

As a credit analyst, I whine when the "moneyness" of debt is ignored. As a structured analyst, my measures of moneyness are based on vintages rather than coincident measures. In general the markets operate without awareness of measurement standards and their abuses. The figure is very suggestive--but it's hard to have conviction about the underlying dynamics at work.

Would love to hear more about the vintages Ann. One thing that brings to my mind is that many are discussing stocks of debt as if they were all made and will all be repaid at today's near-zero interest rates. One of the proximate triggers for the subprime debt crisis was the huge 2/10 ARM issuance with underwriting done on the initial teaser rate period in expectation that the borrower would refinance at the end of two years using the higher house price (house prices always went up!) to qualify for the next 2/10 loan. When prices didn't go up many walked from the loans. That makes me want to underwrite the interest cost of government debt using historical average rates, not current rates. Thoughts?

John, thank you for the 1-minute podium! The analysis of vintages is pivotal in distinguishing securitization from corporate bond analysis. To see how static pool and rolling default measures were conflated in the run up to the GFC is to put that crisis history in very different (and much simpler) perspective. I'd be happy to post something longer on that topic, if it fits your blog. It is a while. And, ultimately it speaks to how Arrow and Debreu missed the point.

What a fantastic idea John (Whine Club!, Ha!) Through my couple decades in the bond market, I've come to the conclusion that its not so much the amount of debt in the economy that's important, rather that of the economy in the debt that is. Therefore, it comes down to just how much potential that debt represents. My own theory of surplus productivity has led me to believe that economic potential (both labor & parts potential) has been grossly under-measured. Therefore, I think a better chart would be debt to potential GDP and I think that measure is very low, perhaps lowest ever recorded. Problem is, we don't have a good way to measure total potential GDP, yet. (Labor Force + Productivity ignores parts potential) All you PhD economic students looking for a dissertation topic, have at it!

Great idea Paul. The economics profession is still stuck in the rising marginal cost curves in the textbooks even though, at least since Brian Arthur's work, it is clear that all information-driven output shows decreasing costs.

A standalone budget deficit is not a problem, nor is debt or printing money on occasion. The important question is what we do with all the liquidity. If it's used for productive capacity rather than just inflating asset prices, it's not a big issue. However, as the chart illustrates, we haven't had a budget surplus in a couple of decades and we have become so addicted to fed supported liquidity injections, bailouts, handouts etc. that we cannot fathom higher interest rates anymore or that the money spigot would dry up one day. These deficits are way past temporary measures, they look more and more permanent.

Remember the taper tantrum? The sheer mention of scaling back asset purchases caused havoc. Too much leverage can be devastating; I know this first-hand as a derivatives trader. When everyone borrows and only the central banks provide liquidity, we have a disaster in the making. As Dean pointed out in an earlier comment, kicking the can down the road seems to be the modus operandi until that can reaches a cliff.

Restrict/taper bank lending so that money creation isn't used for asset purchases. Look at Germany. Thousands of small banks that lend regionally to businesses so that they can buy tech/equipment to be competitive. They have the highest export per capita in the world ahead of China, which has an absolute advantage in total exports. Point is, invest in businesses and not asset acquisition which leads to bubbles. Remember Japan in the 90s?

19% is undoubtedly high. By the looks of the graph it is the highest since WWII. Here are some thoughts in response to the proposed question... In general, over indebtedness is bad and could lead to pressure to default or to print more money. To curb the deficit government will have to increase taxes, which they already plan on doing. The other option to print more money might induce an increase in inflation expectations, and probably will given the current state of household liquidity...this is not good for capital markets. Increases in taxes and the cost of living are also not good for the real economy in the short run. After WWII production was the key to reducing the deficit. Leading to the idea that we could potentially innovate or invent our way out of the deficit. Innovation and invention lead to higher profitability and production thereby creating a larger tax base reducing the pressure to print money or raise tax rates. It will be especially interesting to see how Biden's fiscal plans will impact innovation and production in certain industries in the US. If we don't innovate or produce our way out of this we may see more policy centered around contraction and austerity as opposed to expansion and prosperity of the past decade. Rocky road ahead? Only time will tell.

So many implications. $25.281 Trillion of debt is about 112% of projected 2021 GDP. All seemingly priced to perfection. With the 30 year Treasury yield of 2.3%, what does this portend for future growth and inflation? The three D's; demand, demographics and debt seem to work in consort.

In my corporate finance class we learned about payback periods. Thinking about the analog, the “pile up” period, tells me if we do this for five years we will have “piled up” 100% of GDP in debt (on top of what’s already out there.). What’s the payback period on the accumulated debt? My belief is we will pursue this policy until we are bankrupt, at which time we will reset everything under the guise of issuing a digital currency.

Oh, and on the implications of the chart: a budget deficit of 19% at a time of notional peace makes me think of Argentina, not the US. It will return to historical range when, but not before, a serious President is voted into office that understands how nations turn to ruin and decides not to take that route. If it doesn't, financial ruin follows. Don't cry for me, Argentina.

Great idea, the whine club...

As a former rating analyst (sovereigns and corporates), I whine about how people think that interest rates are going to remain low forever. I've seen too many companies that are 200 basis points from insolvency, and too many countries who will lose their ability to actually have any discretionary spending because a 200 basis point interest rate increase for their debt will quickly force them into a strait-jacket of debt servicing.

I whine that no one seems to remember that debt is future consumption denied (Eugen von Böhm-Bawerk).

I whine that economists have forgotten entirely that economics is a living thing, and to live implies both imperfection and change (Lüdwig von Mises).

I whine that productivity is vastly underreported because even the best hedonic deflators fail to capture the improvements in quality of life and work.

I whine that no one went to jail for the sheer insanity of sub-primes, least of all anyone from the rating agencies.

I also whine about how hard it is to get back into shape after the age of 50, but not even my wife listens to that one.

John, I bow before you and declare you to be the one and rightful Whine-master General for your all-encompassing summary. Each one of them could be an essay in its own right. I look forward to discussing them with you along the way.

I'd vastly prefer to be the Winemaster General... Looking forward to the discussions going forward as well. :-)

As a credit analyst, I whine when the "moneyness" of debt is ignored. As a structured analyst, my measures of moneyness are based on vintages rather than coincident measures. In general the markets operate without awareness of measurement standards and their abuses. The figure is very suggestive--but it's hard to have conviction about the underlying dynamics at work.

Would love to hear more about the vintages Ann. One thing that brings to my mind is that many are discussing stocks of debt as if they were all made and will all be repaid at today's near-zero interest rates. One of the proximate triggers for the subprime debt crisis was the huge 2/10 ARM issuance with underwriting done on the initial teaser rate period in expectation that the borrower would refinance at the end of two years using the higher house price (house prices always went up!) to qualify for the next 2/10 loan. When prices didn't go up many walked from the loans. That makes me want to underwrite the interest cost of government debt using historical average rates, not current rates. Thoughts?

John, thank you for the 1-minute podium! The analysis of vintages is pivotal in distinguishing securitization from corporate bond analysis. To see how static pool and rolling default measures were conflated in the run up to the GFC is to put that crisis history in very different (and much simpler) perspective. I'd be happy to post something longer on that topic, if it fits your blog. It is a while. And, ultimately it speaks to how Arrow and Debreu missed the point.

I would love it Anne and will get it to as many eyeballs as I can. John

(...is a whine--but is a while too)

What a fantastic idea John (Whine Club!, Ha!) Through my couple decades in the bond market, I've come to the conclusion that its not so much the amount of debt in the economy that's important, rather that of the economy in the debt that is. Therefore, it comes down to just how much potential that debt represents. My own theory of surplus productivity has led me to believe that economic potential (both labor & parts potential) has been grossly under-measured. Therefore, I think a better chart would be debt to potential GDP and I think that measure is very low, perhaps lowest ever recorded. Problem is, we don't have a good way to measure total potential GDP, yet. (Labor Force + Productivity ignores parts potential) All you PhD economic students looking for a dissertation topic, have at it!

Great idea Paul. The economics profession is still stuck in the rising marginal cost curves in the textbooks even though, at least since Brian Arthur's work, it is clear that all information-driven output shows decreasing costs.

A standalone budget deficit is not a problem, nor is debt or printing money on occasion. The important question is what we do with all the liquidity. If it's used for productive capacity rather than just inflating asset prices, it's not a big issue. However, as the chart illustrates, we haven't had a budget surplus in a couple of decades and we have become so addicted to fed supported liquidity injections, bailouts, handouts etc. that we cannot fathom higher interest rates anymore or that the money spigot would dry up one day. These deficits are way past temporary measures, they look more and more permanent.

Remember the taper tantrum? The sheer mention of scaling back asset purchases caused havoc. Too much leverage can be devastating; I know this first-hand as a derivatives trader. When everyone borrows and only the central banks provide liquidity, we have a disaster in the making. As Dean pointed out in an earlier comment, kicking the can down the road seems to be the modus operandi until that can reaches a cliff.

As Wiley Coyote found out, there actually is a cliff. /Users/drjohnrutledge/Desktop/th-3.jpeg

Restrict/taper bank lending so that money creation isn't used for asset purchases. Look at Germany. Thousands of small banks that lend regionally to businesses so that they can buy tech/equipment to be competitive. They have the highest export per capita in the world ahead of China, which has an absolute advantage in total exports. Point is, invest in businesses and not asset acquisition which leads to bubbles. Remember Japan in the 90s?

19% is undoubtedly high. By the looks of the graph it is the highest since WWII. Here are some thoughts in response to the proposed question... In general, over indebtedness is bad and could lead to pressure to default or to print more money. To curb the deficit government will have to increase taxes, which they already plan on doing. The other option to print more money might induce an increase in inflation expectations, and probably will given the current state of household liquidity...this is not good for capital markets. Increases in taxes and the cost of living are also not good for the real economy in the short run. After WWII production was the key to reducing the deficit. Leading to the idea that we could potentially innovate or invent our way out of the deficit. Innovation and invention lead to higher profitability and production thereby creating a larger tax base reducing the pressure to print money or raise tax rates. It will be especially interesting to see how Biden's fiscal plans will impact innovation and production in certain industries in the US. If we don't innovate or produce our way out of this we may see more policy centered around contraction and austerity as opposed to expansion and prosperity of the past decade. Rocky road ahead? Only time will tell.

So many implications. $25.281 Trillion of debt is about 112% of projected 2021 GDP. All seemingly priced to perfection. With the 30 year Treasury yield of 2.3%, what does this portend for future growth and inflation? The three D's; demand, demographics and debt seem to work in consort.

In my corporate finance class we learned about payback periods. Thinking about the analog, the “pile up” period, tells me if we do this for five years we will have “piled up” 100% of GDP in debt (on top of what’s already out there.). What’s the payback period on the accumulated debt? My belief is we will pursue this policy until we are bankrupt, at which time we will reset everything under the guise of issuing a digital currency.

We have heard the expression of kicking the economic can down the road for decades. At what theoretical point does the can reach the cliff?

Just like Wiley Coyote in the Roadrunner cartoons you only find out where the edge of the cliff is after you have just stepped off of it.