Summary: Our topic today is real interest rates. In this post we discuss two ideas from my published papers. The first is that, viewed through the lens of Asset-First Economics, the right way to define and measure real interest rates is the difference between market interest rates and tangible asset inflation, not the CPI. The second is that central banks using the wrong measure have caused great damage. That’s how the BOJ triggered Japan’s Lost Decade.

Investors who understand these ideas have a real advantage over those who don’t.

Academia.edu has produced the above audio review of one of my academic papers as a simple summary of the main ideas. You can download the original source article from Academia.edu or by clicking the following link. A transcript of the audio file is below. You can find more information on our Asset-First Economics podcast and video series at www.safanad.com. An archive of my written work is available at drjohnrutledge.substack.com.

I hope that you enjoy the podcast. As a teaser, I will tell you that the logic in this paper was the source of the greatest single trade I have ever made. The long U.S./short Japan bet that Deborah Allen and I outlined in our book Rust to Riches in 1989 had a 16.8x return (25% per year) over the next thirteen years. As always, I welcome your questions and comments.

I have copied the (unedited) transcript of the audio file below in case of interest.

Dr. John

Transcript of audio file below

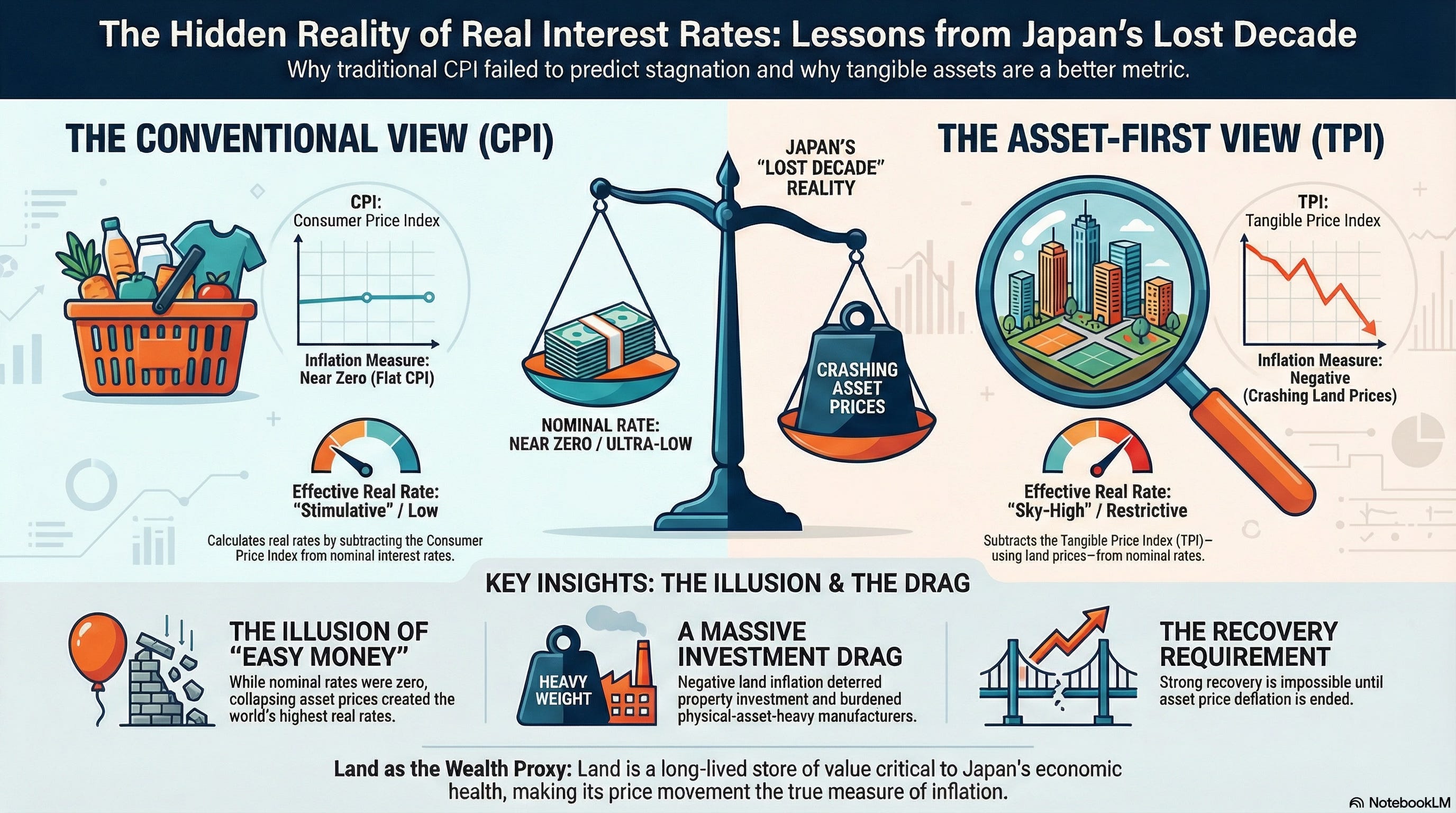

Welcome to Asset First Economics. Today’s topic is real interest rates. Standard measures that subtract CPI Inflation from a market interest rate get it wrong. The right way to measure real rates is to use tangible asset inflation in place of consumer prices. In Japan’s last decade, the Bank of Japan pushed interest rates to zero, but prices of tangible assets collapsed and effective real rates were sky high.

I hope you enjoyed the discussion and welcome your comments.

Dr. John.

Welcome everyone to another episode of In Depth With Academia. I’m Richard Price, your host and the founder of academia.edu, and I’m here today to walk you through a fascinating of work, one that well might seem a little technical at first, but I promise there’s something pretty important here for all of us, no matter what your background is.

the paper I’m diving into today is by Dr. John Rutledge, and it looks at Japan’s real interest rates during its so-called lost decade plus, the extraordinary financial strategies and misguided policies that shaped the economic history of, one of the world’s largest economies.

What’s the main question? Dr. Rutledge tackles Why did Japan stay stuck in deflation for so long? Despite ultra-low interest rates and frankly, Herculean efforts by its government and central bank to pump up the economy? And more importantly, what should we actually make of real interest rates is the way most economists measure them actually capturing what’s happening in the real world.

That’s not just a technical puzzle for economists. This is the kind of thing that influences your investments, your pension, even your job security. If you’re part of this global economy, so why does this matter to you? Well, understanding what drives economic growth or contraction affects decisions about saving, buying property, taking out loans, and even how governments try to get us out of recessions.

If the story we tell about interest rates and prices is off base, it means a lot of policies could, um, actually make things worse. Now let’s dig into the heart of Rutledge approach. Here’s the deal. Most economists and the Bank of Japan at the time assumed that if you set low nominal interest rates, you’re making money easy to borrow and therefore stimulating the economy.

Hold on. Maybe you’re looking at the wrong measurement. Instead of focusing on nominal rates or using the consumer price index, CPI to adjust for inflation, we should be paying attention to the gap between returns on financial assets like bonds, and returns on real tangible assets.

Think land buildings, commodities that people use to store wealth into the future. rather than subtracting CPI inflation from the nominal rate to get a so-called real interest rate, Rutledge suggests using something called the TPI or Tangible Price Index, which in his work he proxies with Tokyo land prices.

Because land is long lived, holds a ton of value and is critical for wealth in Japan and. Get this. While CPI based measures suggested money was easy, the real rates based on uh, tangible assets were actually the highest in the world. People just didn’t want to buy property because prices were still falling, and that creates a massive drag.

I want to pause for a second here because. Honestly, it’s a bit weird to think about, like, do you ever think about how the value store aspect of wealth, whether that’s stocks, gold, How that storage of value plays into economic cycles. In Japan’s case, the negative land price inflation made people not want to invest. Not want to take risks and made it hard for businesses, especially manufacturers who hold lots of physical assets to keep their heads above water. Rutledge argues that Japan’s Central Bank actually kept monetary policy way too tight because they only looked at interest rates and inflation through a textbook Keynesian lens. Rather than understanding the real world asset-based mechanisms, Keynes himself described, especially in chapter 17 of his general theory, if you’re a Keynes nerd, that’s a fun rabbit hole, by the way.

Okay. The key finding here is that high real interest rates based on tangible assets explain Japan’s stagnant growth. And more critically, that ending deflation would probably add at least two percentage points to Japan’s growth rate. Policymakers actually measured and targeted these sorts of real returns.

They’d realize that until asset price deflation ends, there’s basically no hope for strong recovery. So for you, the listener, what does this mean? Well, first question, assumptions. Just because the numbers say easy money doesn’t mean people are actually incentivized to invest or spend. It depends on what’s really happening with the assets that matter in your life.

And second, seeing how academic research questions established measurement methods can make us all a little more humble or maybe just a little wary of claims about economic certainty. As always, remember, I’m not endorsing the view here. Dr. Rutledge perspective is one lens, and like all academic research, it invites us to keep exploring questioning challenging.

Thanks for joining me on in depth with academia. If this episode made you think about Japan money. Or, maybe just made you want to check your own savings, you’re in the right place. and until next time, keep exploring the incredible, imperfect world of academic thought.

Thank you for listening to Asset First Economics. You can find more information on our Asset First Economics podcast and video series at www.safanad.com, and you can find the complete downloadable archive of my written work at Dr. John Rutledge dot substack.com.

Dr. John