How the Dividend Tax Cut Increases Growth

(12/6/2005)

NOTE TO READERS: I have reposted this Golden Oldie from 2005 because it may be the first place I ever wrote down the workings of the asset-centric general equilibrium model that has driven my work for decades. Hope you enjoy.

As my old friends know, I am a big fan of making sure you distinguish between asset markets and flow markets when thinking about the economy. The reason is pretty simple. GDP is a number of about $12 trillion, chump change in comparison with our $155 trillion asset market, including $105 trillion in financial assets and $50 trillion in real estate and other tangible stuff, according to the most recent Fed Flow of Funds reports.

Bottom line: if a policy does not impact the asset markets it does not matter.

Aside: This is no different than asking whether the earth orbits the sun or the other way around. Most people know the sun is the big dog in this story, therefore the earth orbits the sun. Actually this is not true. You can get a free drink at a cocktail party by telling people that actually both the sun and the earth rotate the center of mass of the sun-earth system, which is a point inside the sun but not its center.

This is important because almost all of what passes for macroeconomic analysis today is simply descriptions of who is spending how much money in the GDP accounts. That analysis leads these thinkers to make big mistakes, which gives us great opportunities to make money.

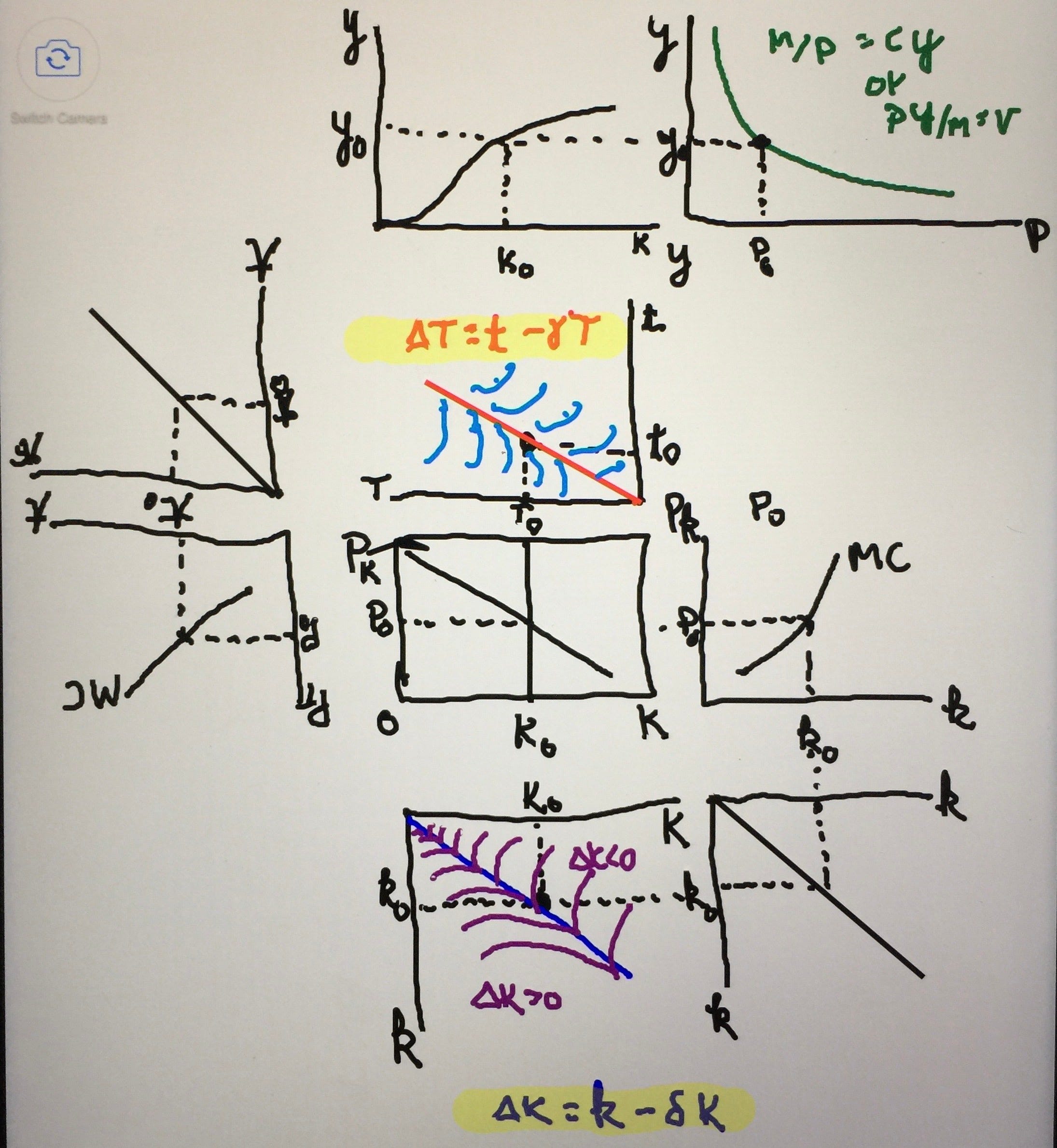

Regarding real estate, take a look at the following diagram.

(Note to Reader: The graphic in the original post has disappeared into cyberspace so I have substituted a more recent one. The graph referred to in the paragraph below is the middle one in this version of the chart. Hope you can follow the remaining text. I will write all of this up more carefully soon.)

In this diagram, the graph on the upper left represents the asset market in which the price P of the existing capital stock, K, is determined.

The graph on the upper right represents the new capital goods (flow) market in which the price of an existing machine, or other unit of capital interacts with the marginal costs of machine manufacturers to determine the number of machines that will be built, which we denote by lower-case k.

The lower right graph is simply a device for bringing big K and little k together on the same graph, which I have placed in the lower left. That is where all the action takes place.

Start with capital stock K(0) and demand for machines D(0) which determine the initial price of a machine at P(0) in the upper left graph. A reduction in the tax rate on capital increases the number of machines demanded at each price, creates an excess demand for homes, and pushes the price of an existing hime up to P(1). This is the initial re-pricing impact of the tax cut.

In the new machine market in the upper right graph, the higher machine price results in more machines being built per year, k(1), than was the case at higher tax rates.

Now the hard part. The graph in the lower left is a phase diagram, a concept we can use to help think about dynamic change over time. The critical concept is the stationary state line descending from the origin downward and to the right. That line represents combinations of K(t) and k(t) that leave the existing capital stock unchanged. This will happen when the construction of new machines, k(t) is just big enough to replace the number of machines that have worn out that year through depreciation . I have assumed that of existing machines depreciate by delta percent each year. For example, if a machine lasts 14 years, then delta would be 7% per year.

Assume we start at K(0) and k(0), which is a point on the line described above, i.e., we start in a situation where the capital stock is neither growing now shrinking. I can do this--it is my chart!

Now lower the tax rate on capital income. The higher demand in the upper left graph increases the price to P(1), which increases machine production in the upper right to k(1). But at k(1), we are building more machines than needed to replace the ones wearing out. Therefore the capital stock is growing. In fact, a little thought and 2 glasses of wine will convince you that all the points downward and to the left of the line in the lower left graph represent situations of a growing capital stock. In fact, the distance from the line indicates how fast it is increasing. Conversely, all points to the right of the line represent a shrinking capital stock. The capital stock will continue to grow until machine production and depreciation are once more equal and the capital stock is in a new, larger, stationary state. (Geek note: Ludwig von Mises would have referred to such a point as an evenly rotating economy. Richard Dawkins and other ethologists and system theorists would call them ESS, or evolutionary stable systems.)

A drop in tax rates on capital income will make an initial spike in machine prices but, over time, the growing capital stock will mitigate some of the price pressure, which means the initial burst of activity, and possibly of price, are likely to moderate somewhat over time. To an information theorist the initial spike in price is a way of amplifying the initial information signal that capital is now scarce in order to get everybody's attention so they get to work and build more capital goods.

So tax cut induced capital inflation is largely a one-time event, but at a permanently higher capital stock. This leads to permanent increases in productivity and incomes, and barring any subsequent change in monetary policy, to a permanently lower price level.

This story would play out in reverse if there were a sudden reversal of tax rates. The result would be a drop in capital goods prices, reduced investment, a shrinking capital stock, and slower productivity and income growth.