Friday Brain Dump

Corrected August PCE 1.6%. Springtime in New York. Things that are not a thing.

Note to Readers: I posted this piece late Friday night and am reposting Monday morning for those who missed it over the weekend. I apologize if you have already seen it, in which case I advise you to press the DELETE key on the top right corner of your keyboard.

Summary: Corrected August PCE inflation was 1.6%, not 2.5%—Fed needs to keep cutting. Spring is in the air in New York—commercial real estate moguls I met with this week are sharpening their knives for later this year when they expect thawing credit markets to spike foreclosures and discount sales. First few of my “things that are not a thing.” Please use the Comments button help me add more.

Corrected PCE Inflation 1.6%

In my last post, I explained that the corrected August 12 month CPI inflation rate, after removing Owners’ Equivalent Rent (OER), was just 1.4%, not the 2.5% in the official report. Making the same correction for OER bias to the Fed’s favorite inflation measure, PCE, in this week’s August Personal Income and Outlays report reduces August inflation from 2.5% to just 1.6%. Corrected PCE inflation has averaged 1.6% over the past 3 months—past time to start cutting rates.

Spring is in the Air

My calendar tells me it is the first week of October, but there is a whiff of springtime in the air—maybe even two whiffs! I’m in New York at Safanad this week having conversations with an extraordinary lineup of private equity, credit, and commercial real estate investors. Now that the Fed has changed directions and interest rates will be heading lower for at least the next two years, they are all starting to think about how to position their portfolios for the eventual thawing of the credit market and associated turnaround of commercial real estate that is already starting to happen.

That counts on rates continuing to decline, of course, but I think that is a safe bet. The Fed waited too long to start cutting rates but surprised me when they chopped 50 basis points off the rates last week. (I didn’t think they had the nerve—or the good sense—to do it.) The cut will help floating rate borrowers to some degree but will reduce the incomes of the people who own our $6.5 trillion in Money Market funds by $32 billion per month, which almost exactly erases the $34.2 billion increase in disposable income for the month of August so don’t look for a jump in economic activity just yet.

The fact that bond yields went up, not down, tells us that 50 bps. wasn’t enough. They need to do another 50 right away and another 100 as soon as they have time to hike up their pants again. We need 3% interest rates, not 5% rates, to bring bond yields down enough to rejuvenate the underwater assets on regional bank balance sheets and get the credit markets open for business again.

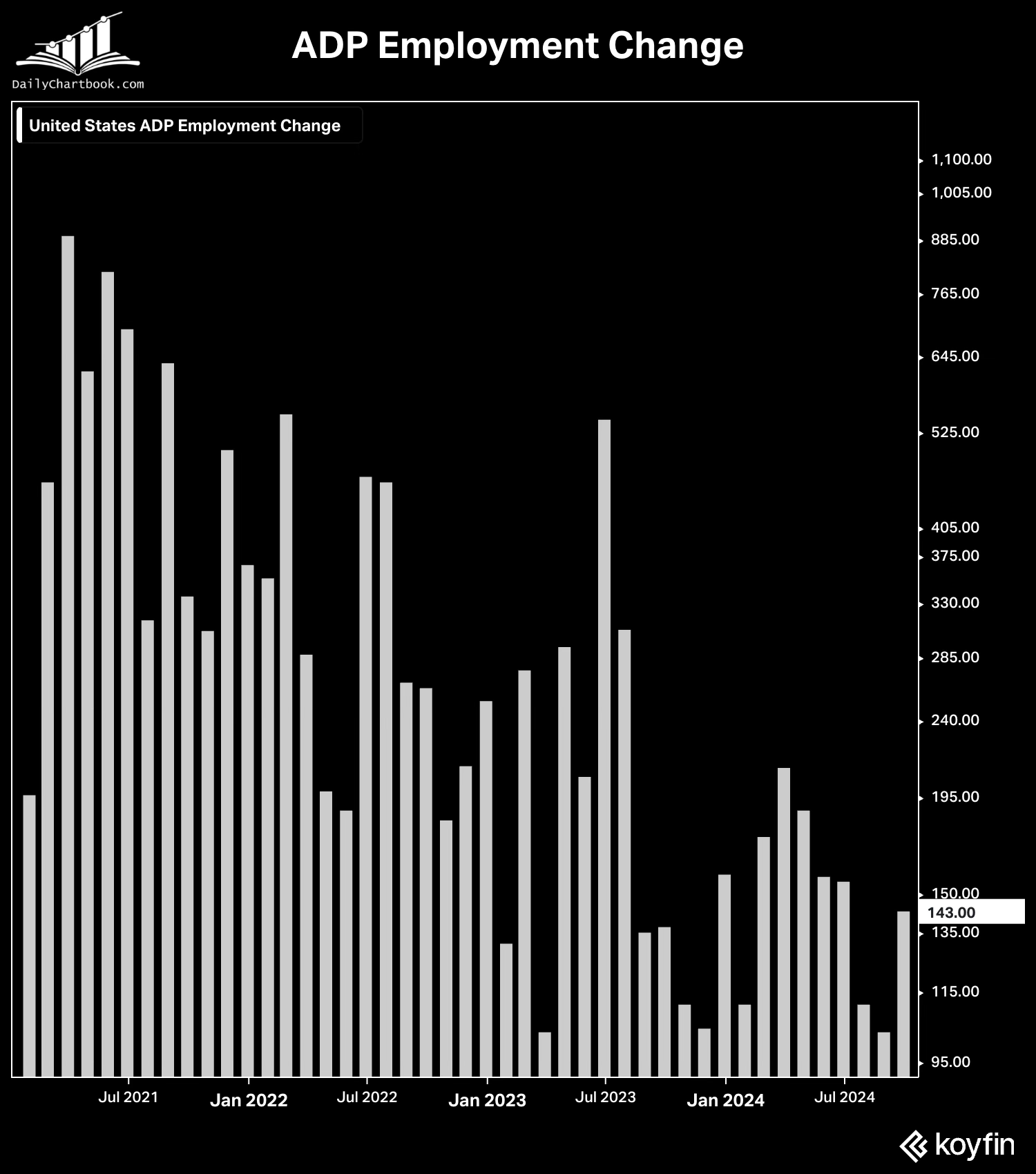

This week’s employment reports told us that economic activity is doing well, but it will do even better when rates drop below 4% next year on their way to 3% and credit markets open up again. And make no mistake—credit markets are still closed for small business customers of regional banks. Bank commercial and industrial loans—$2779 on September 18—billion were $21 billion lower than they were 21 months ago, in January 2023.

That explains why this week’s ADP report showed that in September, even though total job gains (+143K) were strong, businesses with less than 50 employees lost 8000 jobs.

Today’s Employment Report confirmed ADP’s strong job growth story. Nonfarm payrolls added +254K jobs in September and July/August were revised upward by +72K, amounting to +326K total new jobs against a +203K average over the past year.

Strong job growth, falling interest rates, and a thawing credit market are all good for investors. As credit markets thaw out, there will be some interesting opportunities in small cap stocks, in credit, and in commercial property.

Today, many regional and community banks are in “extend and pretend” mode (also known as “a rolling loan gathers no loss.”) By extending the maturity date on an unrefinancable commercial property loan, a bank can avoid taking over the property and writing down the loan and the borrower can avoid a forced sale that would wipe out his equity. As credit the markets thaw, however, and banks see potential buyers for foreclosed properties, some of those forced-sales are going to happen, allowing cash-rich value investors to buy good properties at deep discounts. But remember, to be a cash-rich value investor you have to have cash, so you need to be patient.

My Favorite Whine—Things That are Not a Thing

Thinking is hard work, which may be why people go to such great lengths to avoid it. Jargon is the short-cuts that people use to suppress thinking and questions about issues they think are already decided. At best, jargon saves time by compressing a paragraph into a single word. At worst, it channels all subsequent mental activity into well-worn grooves, leading to a kind of group-think, more like a religious mantra than analysis. Unfortunately, when the world gets complicated jargon-users rarely know how to rewind the tape and rethink the basics. That’s why I try so hard not to use jargon in the things I write.

I think of jargon that no longer makes sense as things that are not a thing. Here are some of the terms on my “things that are not a thing” list:

Modern anything. Referring to your own thinking as “Modern” takes a special kind of hubris because it basically says that all of the ideas that have come before were just the on-ramp to the correct way of thinking—the way that you do it now. That is true for Modern Portfolio Theory, for Modern Macroeconomics, and for Modern Monetary Theory, referring, respectively, to the illusions that you can control risk, that you can control the economy, and that you can print all the money you want without creating inflation. None of them are true.

Optimal Portfolio. The illusion that you can measure the risk of owning an asset by calculating the standard deviation of its trailing returns and their correlation to the returns on other assets is a load of bunk. IMHO, risk is the likelihood that the thing you bought doesn’t generate the cash flow you thought it would when you bought it, which is a different beast altogether.

Risk-On, Risk-Off. These are terms people made up to explain away the times when the correlation coefficients they use to build so-called optimal portfolios don’t stay put. Correlation coefficients and covariances are not facts of nature; they are accidents of history. They are more like your brother-in-law; never there when you need them.

Alpha, Beta. These are terms that only have meaning if you have already accepted the jargon I have already talked about. I don’t, which is why I never use those terms.

r*, or R-Star. This is a term that macroeconomists and Federal Reserve officials use to refer to some magical interest rate that would be “just right,” like the baby bear’s bowl of oatmeal in Goldilocks, leading to both full employment (general equilibrium) and no inflation. Fact is, r* only has meaning if you have already accepted Modern Macroeconomics (see thing #1 above), an economic model built on the idea that only one person in the economy, who is really smart, and that you can ignore the balance sheet that, in the real world, is more than 15x bigger than annual GDP.

Space, as in “This is the fastest growing company in its space.” Call me old fashioned but, to me, space is either a place to park your car, as in “parking space” or it’s a frontier where no man has ever gone before, like in Star Trek. It is not a code word for an industry or an economic sector. The first time I ever heard it used this way was in 2001, at the height of the dotcom bubble, when an investment banker brought a high school senior to my office who wanted $10 million so he could use the internet to build an online shopping mall that would “redefine the retail space.” It was a short meeting.

These will do for a start; I will be adding more to the list in future posts. I am very interested in your thoughts on jargon that should be on my list. Please use the comments button below to let me know your thoughts.

Reach out is bad English, making no sense regarding a conversation. How about "I will call"

I love how you write. By the end of the year, I'm going to keep up with your articles and read as many of your previous articles as I can to gain an understanding of Economics. Thank you so much for this opportunity!